Banking Governance & Culture Report Series:

Part 4 (of 10)

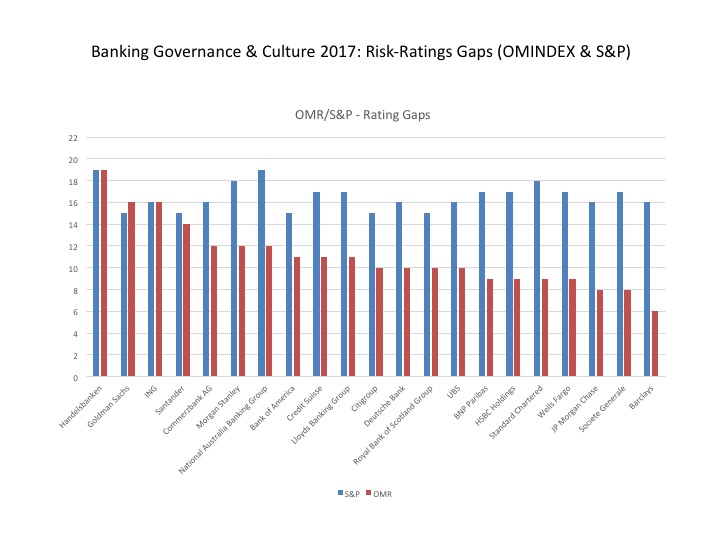

Bank OMINDEX ratings contrast with credit ratings as an indicator of organisational health

“Just before the crash of 2008, when S&P and other credit rating agencies, were awarding RBS a ‘AAA’, the CFO of RBS was reporting excellent profits. Yet the whole edifice of the bank had already started to crumble; ignorant of the risk that had already materialized in the form of its toxic mortgage book.” 2017 Banking Governance and Culture Report

The most visible sign of governance and culture risk arises from misconduct, something firmly on the agenda of regulators and reported extensively in the media. Most organisations that have suffered from serious misconduct often express this as arising from “rogue” employees. In reality, they suffer from ‘rogue’ human systems, which only come to light and are often later admitted to after the full financial consequences are discovered.

Yet most risk goes unseen. Each day, organisations are seeing significant value eroded by poor governance and ineffective human capital management. Unacceptable customer service that damages a brand, failure to utilise existing knowledge to improve or innovate, and ill-conceived decision making that fails to make the best strategic choices, are but a few.

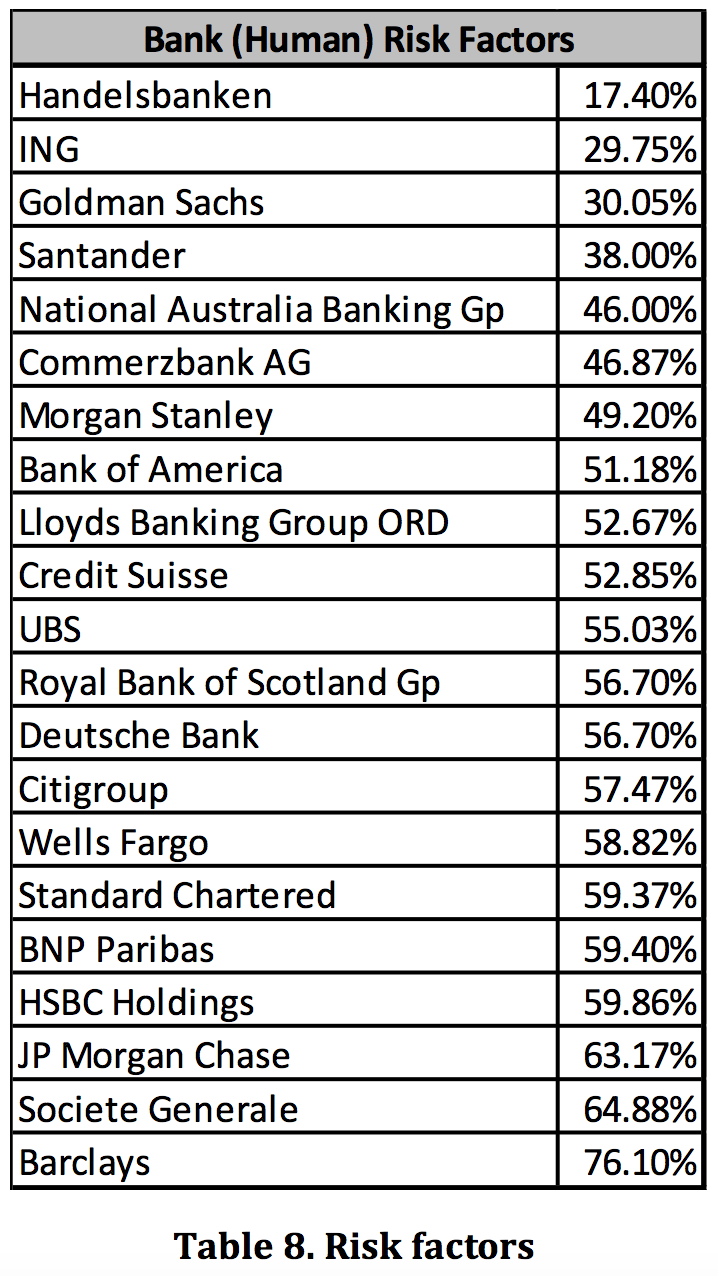

Our analysis provides an elegant solution to the question of balancing both sides of the value/risk coin. The OMR score (%) and Risk Factor (%) for any organisation will always come to 100%. For example, Barclays OMR score of 23.90% produces a risk factor of 76.10% (a total of 100%).

The OMR Risk Factor is specifically designed to incorporate the probability of any company carrying undetected, material risk with respect to its governance and culture (G&C). It serves as a predictive, long-term indicator of risk that could manifest as catastrophic value collapse but will also identify ongoing value erosion.

Governance and culture risk arises out of equivocal, unclear or skewed organizational purpose and values that permeate all company systems: from decision-making, resourcing, reward, learning and performance management to quality assurance. Only by understanding risk in this context is it possible to fully understand and predict the likelihood of corporate problems and failures.

Governance and culture risk arises out of equivocal, unclear or skewed organizational purpose and values that permeate all company systems: from decision-making, resourcing, reward, learning and performance management to quality assurance. Only by understanding risk in this context is it possible to fully understand and predict the likelihood of corporate problems and failures.

One overall finding in terms of the banking sector’s ability to manage G&C risk is that banks do not understand, nor appreciate, the whole system nature of the problem. More worryingly, despite the slew of misconduct costs that have arisen since the GFC, a number of banks remain incapable or unwilling to identify and confront the underlying root causes of inappropriate behaviours.

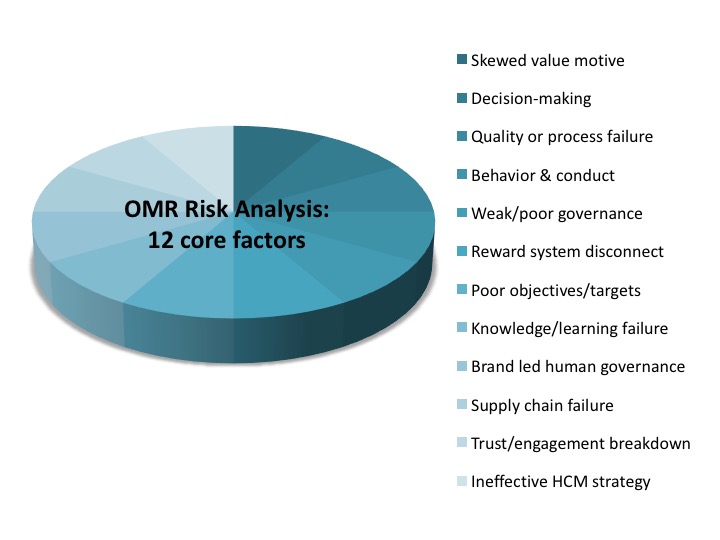

The 12 Governance, Culture and Human Capital Risk Factors

This must change. Our approach is to use a whole system Governance & Culture risk analysis, integrated as part of our OMR methodology, to identify the nature and quantum of business risk that is inherent within an organization. This involves analysis of twelve core, and interrelated governance, culture and human capital factors that have causal connection to material business risk. Our full findings for the banking sector, which should be an essential read for boards, investors and regulators can be found in our 2017 Banking Governance and Culture Report.

Comments are closed