Have you ever been asked to take an oath? Did any business school act like a medical school and demand a Hippocratic allegiance before you graduated? Perhaps we just don’t take corporate leadership seriously enough?

Have you ever been asked to take an oath? Did any business school act like a medical school and demand a Hippocratic allegiance before you graduated? Perhaps we just don’t take corporate leadership seriously enough?

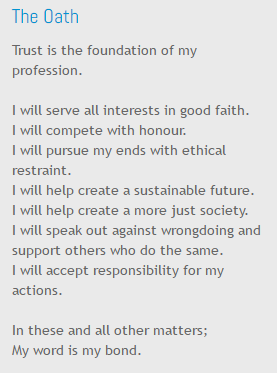

I have just taken an oath – the Banking & Finance Oath. This was a very personal choice and a very serious decision on my part. It was a good feeling. I now want to engage with others who share the same values and whose leadership and management practice are equally principled. So why did I decide that it was important to take this Oath?

At MI, we are putting the final touches to our Banking Governance & Culture Project, which has researched and rated 21 global banks. No one has ever made such an undertaking before; with every bank being assessed against a common standard. National governments of every hue, and their banking regulators, will talk about getting the ‘banking system’ back under control but any pretence that a global banking system actually exists is wafer thin. The reality is much more akin to sector made up from a disparate group of actors, all running their own agendas. Anyone wanting to bring some order to this gathering will first have to install the minimum requirements that define a system. These are: –

- A common purpose

- A set of rules agreed (and followed) by all players

The present banking arrangement fail on both these criteria so building a legitimate and robust banking system has to begin with a declaration of common purpose from all of the world’s banking Chairs and CEOs and all of their regulators. What we have already learned from our Project is that very highly qualified corporate lawyers, from a range of jurisdictions, have informed us that the legal position on corporate purpose is not as clear cut as it could be. This might explain why so many of the banks on our research list have such differing views as to why they exist.

For example, if we compare Goldman Sachs with ING, there is a stark contrast about who comes first in the pecking order of purpose: one favours shareholders while the other sees its ultimate purpose as serving society. These two goals cannot be mutually exclusive. In MI’s philosophy they are not only mutually inclusive but inseparable. By serving society first, banks can regain legitimacy and provide shareholders with the best returns possible. That is the standard by which all corporations are rated on OMINDEX and their real value is measured in terms of Total Stakeholder Value.

This helps to explain a very interesting finding that will feature in our final Project Report; Goldman and ING both achieved exactly the same OMR rating (score). This means that these two banks can think they are in the same sector, doing similar things and towards the same end, without actually realising just how differently they are behaving. Goldman’s relatively high rating is primarily due to it being very good at producing value. However, that does not automatically make it ‘societal’. Conversely, ING appear to live and breathe ‘society’ but they could learn a lot from Goldman’s about how to generate more value. In other words, OMR ratings do not subscribe to the simplistic view that banks are either ‘good or bad’. The reality is just a very human range of confusing purposes and relative capabilities. Without a common purpose though, banking leaders are making a highly complex environment needlessly complicated.

Of course, when a Maturity Analyst starts researching banking behaviour in some detail, using a standard instrument such as the OM30, all of the complexity disappears and order can be restored. For example, when we first rated Deutsche Bank in 2015 we gave them an OMR of B+ and regarded them as a possible ‘basket case’. At the same time their S&P credit rating was AA. We call this the risk/rating gap between conventional financial analysis and maturity analysis. Since then S&P’s rating has been downgraded to A- while our latest OMR for Deutsche Bank has risen to BB-: still low but at least on a slightly better trajectory. One of the reasons for our upgrade is the new CEO, John Cryan, who scores very highly on authenticity. The sort of leader I can personally identify with (he doesn’t believe in bonuses); but he still needs the mature capability to change the culture and value of Deutsche Bank for the long term.

If national governments and their regulators are to have any chance of resolving all of the woes of the corporate world and the capitalist ‘system’ they have created, then first we need to search high and low for people whom we can trust. We can build the right capability for the right purpose as long as those foundations are laid. Fortunately, the world is a big enough place that, if you look hard enough, you will find the right people. When I started my own work as part of our Banking Governance & Culture Project I had to rate NAB (the National Australia Bank) and discovered the existence of the Banking & Finance Oath, which is an Australian initiative. I decided this is exactly what the global banking system needs if it is ever to become a genuine system.

I’m not a banker, but when I read the Oath I had no problem taking it and I believe every Chair and CEO in every sector (private and public) should do the same. I hasten to add, however, that taking the Oath is a very personal choice. I did not take it as the Chair of MI but just as an ordinary (albeit professionally informed) citizen who can see no good reason why banks (or any other corporation for that matter) should be allowed to operate outside of a well-regulated system that is in everyone’s best interests.

Comments are closed